In 2016, Israel experienced interesting and surprising macroeconomic trends. The economy witnessed a higher GDP growth rate than in the previous two years, as well as growth in labor force participation and wages. The question is whether the economic growth of 2016 indicates a return to Israel’s average economic growth rate prior to the global economic slowdown (beginning in late 2011) or whether 2016 is an exception and the economy will return to sluggish growth in the coming years. Brand and Weiss find evidence indicating that 2016 was merely an outlier and that a return to slow growth may be on the horizon.

In the years following the financial crisis, and particularly since 2012, Israel experienced a considerable slowdown in economic growth. Between 2012 and 2015, GDP per capita growth decreased from an historic average of almost 2% a year to an annual growth rate of about 1%-1.2% a year. Israel’s economy improved in 2016 and growth of GDP per capita for the full year, which has not yet been published, is expected to stand at 1.5%.[1] This is a slightly lower rate than in the past, but higher than the two prior years. However, the Bank of Israel predicts that GDP per capita will return to a growth rate of about 1% in the coming years.

There were positive developments related to wages in 2016, as well. Real wages rose by 2.3% in the first three quarters of the year, after a 3.1% increase in 2015. These wage increases are exceptional in comparison to the very low increases in real wages in previous years and are inconsistent with stagnant productivity growth during this period.

When economic growth is broken down into various factors, it seems that the biggest contributor to growth per capita in recent years was the expansion of the labor market, which resulted from a steep rise in labor market participation rates. However, this trend is unlikely to continue in the future for two main reasons: firstly, the share of working-age Israelis is expected to decrease as baby boomers reach retirement and, secondly, further increases in employment are most likely to come from the Haredi and Arab Israeli sectors, where human capital is relatively low or not well-matched to the needs of the modern labor market – thus contributing little to overall economic growth. Therefore, Israel’s economic growth that emerges as a direct result of an expanded labor force is approaching its upper limit and is likely to wane in the coming years.

It is important to note that the increase in labor force participation and decrease in the unemployment rate in recent years is an unusual phenomenon given the sluggish growth in Israel’s per capita GDP, and is due to changes in the composition of demand in Israel’s economy: a shift from exporting industries with high productivity levels to labor-intensive industries, characterized by low productivity.

At the same time that Israel is experiencing a sharp rise in employment rates, there has been a decrease in investment in capital (such as infrastructure, machinery and equipment) and a slowdown in the growth of human capital. Although the data show an increase in investments during 2016 this is largely due to one company (Intel) and does not reflect the rest of the economy. Given low interest rates and a relatively stable economy, it is surprising that investment has slowed in most sectors of Israel’s economy. The danger in these trends lies in the effect they will have on Israel’s potential long-term growth.

The big question that arises from these trends is: why is there not more investment in Israel’s economy? The challenges of investing further in physical capital and human capital may lie in bureaucratic barriers as well as in geopolitical factors.

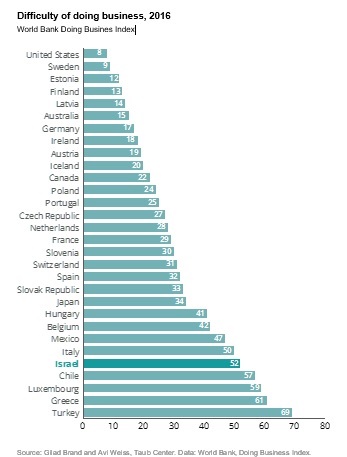

A possible way to drive growth is to improve the business climate in Israel. Each year the World Bank publishes the “Doing Business” report, which ranks countries by the level of difficulty of conducting business there. This index ranks Israel in 52nd place, below nearly all of the other OECD countries. This low rating reflects the need to streamline bureaucracy – especially in the realms of real estate, foreign trade, domain registration, and property tax payments. In these areas, Israel is ranked very low worldwide and requires a dramatic change to support faster economic growth.

Looking forward, demographic shifts in Israel require greater investment in physical capital and human capital, particularly within those population groups that are growing rapidly in size. Increasing competition among local businesses, streamlining bureaucracy, and removing barriers to imports will all help stimulate economic growth in Israel in the long term.

The positive economic growth in 2016 and the good condition of Israel’s labor market make this an ideal time for policy makers to address the demographic and structural challenges facing the economy. The sooner policy makers implement policies based on long-term economic considerations, the easier it will be to promote balanced growth of Israel’s economy.

[1] According to the Bank of Israel, Israel’s GDP is expected to increase by 3.5%, and GDP per capita by 1.5%. The Central Bureau of Statistics (CBS) predicts the GDP will increase by 3.8%, and by 1.8% per capita.

Author

Taub Center Staff

Recent Posts

How is the Life Cycle Funded in Israel?

03.11.2025- Alex Weinreb , Kyrill Shraberman , Avi Weiss

The Importance of Complying with Supreme Court Rulings In Order to Preserve Democracy and Social Welfare

07.04.2025The Taub Center for Social Policy Studies in Israel, an independent, non-partisan, socioeconomic research institute based in Jerusalem, has been

- Taub Center Staff

325 Days of War: Data Compilation of the Northern and Southern Communities

25.08.2024These days mark 11 months since the outbreak of the war. Since October 7th, 1,635 Israelis have been murdered and

- Taub Center Staff

Homicides in Arab Society Continue to Climb

10.02.2025The Taub Center publishes updated 2024 data on homicides across Israel’s population groups. Our concerns have not abated. Our February

- Taub Center Staff