The Hadassah Foundation has provided generous support for the creation and implementation of this study.

For the full publication in Hebrew click here

In recent years there has been much public discussion about a variety of issues relating to pensions in Israel, including concern about the performance of pension funds and the implications of an aging population on the pension system.

A new Taub Center study by Liora Bowers and Hadas Fuchs analyzes pensions from a gender perspective and examines both the labor market and the pension system to assess what pension income gaps between men and women will look like in the future.

Main findings:

- Women’s monthly income from occupational pensions is lower than that of men, on average, due to the fact that women earn lower salaries on average, go on maternity leave, and tend to retire earlier from the labor market.

- Retirement age has a notable impact on pension income – postponing the retirement age from 62 to 67 increases income from occupational pensions by 45% and from old-age allowances by 25%.

- Simulation estimates show that even if women delay retirement until age 67, the gender gap in income from private pensions would still be at least 20% among married individuals and 27% among single individuals. Old-age allowances, however, narrow these gaps: when they are taken into account in the simulation, the gaps are reduced to 13% and 20%, respectively.

- The estimated future gap in pension income between men and women places Israel roughly in the middle of the ranking of European countries.

Pension savings by gender: Men save more – with the exception of Haredim

To estimate the expected pension income for men and women, Bowers and Fuchs examine the various pillars of the pension system in Israel. The system is comprised of three pillars:

- Allowances: The National Insurance Institute (NII) grants an old-age allowance to every individual over the age of 70 (the absolute retirement age), and at an earlier age for employees who retire at the conditional retirement age (62 for women and 67 for men) or for low-income earners. The elderly living in poverty also receive some income support – one in five senior citizens is eligible for this benefit.

- Private occupational pensions: In 2008, Israel implemented mandatory pension coverage and from that time every employee has been obligated to deposit part of their income in a pension fund (as are their employers). The monthly pension payment received during retirement is determined by the sum of money accumulated in the fund.

- Voluntary contributions.

The differences between men and women for each of these pillars are expected to dictate the degree of future gaps in pension income.

Current data from government institutions do not allow us to estimate gender gaps in pension savings today because these data are provided at the household level and do not include distinctions by gender for married couples.

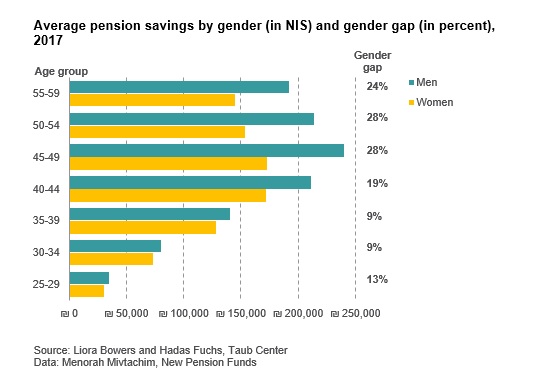

Therefore, the Taub Center study is based on alternative methods of estimation. One of them uses data for 640,000 people who held a pension fund with Menorah Mivtachim (the largest new pension fund in Israel) in 2017. These data do not provide a complete picture of pension gender gaps because they only include individuals insured by the new pension funds, but they provide a rough estimation.

The data indicate that there is indeed a gender gap in private pension savings and this gap increases with age. The most significant gap was found among those aged 45-54: men in this age group have 28% higher occupational pension savings than women.

The study also compares three population groups – Arab Israelis, Haredim, and the remainder of the population – in light of the differences in employment rates and incomes between these groups.

The study finds that in the older age groups (44 and older) the average pension gender gaps are higher among Arab Israelis, but for those aged 44 and under, the expected gaps for this sector are similar to those in the rest of the population.

The smaller gap at younger ages seems to reflect an intergenerational change – for the younger generation, the employment of Arab Israeli women has increased considerably, and, therefore, their pension contributions are expected to be much higher than those of the previous generation.

The private pension savings of Haredi women in the 25-34 age group is 26% higher than that of Haredi men, reflecting the higher employment rates of women in this population group.

What affects women’s pensions? Work hours, childcare, and the Consumer Price Index

The Taub Center study by Bowers and Fuchs also uses a comprehensive index that measures the expected future pension gender gaps in European countries to compare the situation in Israel to that in Europe. The index includes selected employment and pension system data, and, by analyzing these data, the researchers find a number of factors that have a particularly notable impact on the pension gender gap in Israel.

Employment data: Policies in Israel encourage the employment of women; for example, women receive higher tax credits than men. Indeed, the employment rate of women in Israel is relatively high: about 66% among women of working age (a difference of 7 percentage points from men, compared to an average gap of 15 percentage points in the OECD).

Since private pension funds play a very important role in post-retirement income, the higher magnitude of employed women reduces gender disparities relative to the world.

However, other data widen the gap; the hourly wage gap between men and women in Israel falls in the middle of the OECD ranking (standing at about 19% as of 2016), and there is a relatively high gap (16%) between the number of weekly working hours for women (about 37 hours) and for men (about 44 hours).

Continuity of employment: The fact that those who take parental leave in Israel are nearly all women, and that women are usually the primary caregivers for children, is also reflected in the accrual of pension entitlements. Paid maternity leave (15 weeks) is considered an insured period for the purposes of calculating seniority and the accrual of pension entitlements, but if a woman chooses to extend into unpaid leave (as many do), this period is not insured.

In Israel, the protection of pensions during periods of childcare is relatively limited compared to countries in the OECD, most of which have policies for reducing these gaps – for example, through pension entitlements or private contributions for the parent.

A simulation of OECD countries shows that a woman in Israel who leaves her career for five years to provide childcare will receive about 90% of the pension income of a woman who did not take a break, a finding that places Israel in fourth-to-last place in the ranking of OECD countries.

Government allowances: Redistribution policies in the pension system by means of allowances affect the pension gender gap, and provide an advantage for women. A man and a woman who paid NII contributions for at least 35 years and retire at the official retirement age will receive an identical monthly allowance from the NII.

However, every employee has the option of deferring the onset of the allowance until the age of 70 and receiving an additional 5% for every year of delay – and, because of the gap in the conditional retirement age, a woman who chooses to retire at age 70 will receive 22% more than a man who does the same (NIS 3,224 compared to NIS 2,648).

As of 2003, the monthly old-age allowance is linked to the Consumer Price Index (CPI). The CPI rises at a slower rate than wages, and, therefore, pensions are eroded relative to the average income in the economy. Given that women have a longer life expectancy, linking allowances to the CPI affects them more and erodes their pension more over time relative to wages in the economy.

Retirement age: Israel is among the nine OECD countries that have retirement age gaps between men and women, and one of only three that are expected to maintain this gap through 2060. This contributes greatly to reducing women’s pension income relative to men’s; therefore a woman who chooses to delay retirement can increase her occupational pension income by a substantial amount.

The retirement age for men in Israel (67) is the highest in the OECD, and many women continue to work after their conditional retirement age (62). In 2016, 53% of women and 70% of men in Israel aged 65-69 worked, 10 percentage points higher than in the OECD.

Pension payment coefficient: Israel is among only four OECD countries that take into account gender when calculating the monthly sum to be paid to each insured individual in the fund, a practice that is illegal in many other countries. Since the life expectancy of women is higher, pension companies divide the total savings balance in the contributions fund into a higher number of payments – thus, women receive a lower sum each month.

Among married couples the calculation includes survivor’s insurance, making the coefficient almost the same for men and women, but a single woman has a coefficient that is 7.5% higher (and a correspondingly lower monthly pension payment) than a single man who retires at the same age. At the same time, the gender gap in pension provisions directed to life and disability insurance actually slightly increases pension incomes for women, and reduces the gap to 6%.

What will the pension gender gap be in the future?

In an attempt to estimate the extent of the future pension gender gap, the Taub Center researchers conduct a simulation that estimates future pensions based on current average salaries and salary growth for each gender.

Among married couples who retire at the age of 67, a woman will receive about NIS 13,300 a month from a pension (occupational and old-age allowance), while a man will receive about NIS 15,300; that is, NIS 2,000 more than the woman. Among single individuals, the gender gap is even larger, and a woman who retires at the age of 67 will receive about NIS 3,000 less than a man.

Retirement age has a significant impact on pensions: a woman who retires at age 62 will receive about NIS 3,800 less per month than one who retires at age 67, both because of lower total accrual in her pension fund and because she will not receive additional funds for postponing the old-age allowance.

Bowers and Fuchs say that awareness should be raised about the impact careers have on post-retirement income. Fuchs says: “The more people contribute to their pensions during employment, the larger the sum they receives in retirement.

Women in Israel do work at high rates, but men work more years, work more hours, and have higher wages, so their average income is higher than that of women. The key to narrowing the pension gap is narrowing the gaps that exist in the labor market.”

Bowers adds: “In terms of government policy measures, there are ways to reduce pension gaps – first and foremost, to raise the retirement age for women (taking into account the complexity of this issue); to find solutions for maintaining continuity of pension and social security benefits during maternity leave and childcare; and to reevaluate the gender aspects of private pensions, like calculating the coefficient.”

President of the Taub Center, Prof. Avi Weiss, comments: “Policymakers should think about how the distribution of resources will encourage people to participate in the labor market on the one hand and reduce inequality on the other.”