Author

Taub Center Staff

Last month, the State of the Nation Report 2022 was published which presents new data in the areas of economics, the labor market, welfare, health, education, and demography. Prof. Benjamin Bental and Dr. Labib Shami, from the Taub Center, present an optimistic picture of the Israeli economy, which stabilized and returned to its pre-COVID trends. The study reviews the state of the Israeli economy in 2022 and describes the positive developments that began while indicating the structural problems that harm labor productivity and impact the cost of living in Israel relative to other countries.

In 2020, many governments took steps to ease the economic impact of the COVID crisis and significantly increased their deficits and debts. As a result, the ratio of debt-to-GDP in Israel rose similar to that of the OECD average, about 12 percentage points, and reached about 71%. In the Euro Area, the average increase was sharper with an average of 14 percentage points.

The rapid growth in GDP in 2022 and the commensurate increase in government revenues in the first three quarters of 2022 created a surplus of 2.6% in the GDP. By the end of 2022, the debt-to-GDP ratio fell to about 61% — close to its pre-crisis level, and according to estimates by the IMF, by the end of the decade, it should reach about 55%. In this way, Israel will reach the median level of the OECD countries.

An optimistic picture of the Israeli labor market — less unemployment and more job vacancies

In the first few months of 2020 with the advance of the COVID crisis, the unemployment rate in Israel rose with no change in the share of job vacancies. As the unemployment rate began to stabilize at a higher level, there was a parallel and significant rise in the number of job vacancies. By mid-2021, the unemployment rate returned to its pre-crisis level, although there was no similar decrease in the share of job vacancies in the labor market. The ratio between job vacancies and unemployment continued to rise in 2022, and despite a slight decline towards the end of the year, it remained quite high relative to the pre-crisis period.

On the structural side, the review highlights the long work hours in Israel alongside low productivity. In 2019 (pre-COVID), the average number of work hours for an Israeli worker was about 1,900 hours per annum — 25% more than the average in European countries of a similar population size to Israel (Austria, Bulgaria, Denmark, Finland, Ireland, the Netherlands, Sweden, and Switzerland). In terms of labor output, the situation is reversed: in 2021, labor productivity in Israel was about $48 per work hour (in 2017 prices), and in the comparison countries, productivity was higher by about 25%. One of the explanations for these disparities is connected to the levels of public and private capital per employee in Israel, which have not grown since 1980 and remain very low relative to the comparison countries.

Productivity and wages in the high tech sector are significantly higher than in the rest of the market place

In 2021, the high tech industry sector employed about 10% of the labor market employees, and contributed about 15% to GDP. A little over two-thirds of the job positions in the sector are in the areas of service and the rest are in manufacturing. Within the service branch, the rapid increase in the number of positions in programming and the decline in the number of positions in information services stands out. In terms of labor productivity, in the traditional technology industries, from 2004 to 2022, the average number of work hours decreased by about 20% and productivity grew by about a quarter. In contrast, in the high tech industry, outputs rose by about 170% while the number of work hours increased by only about 20%. The rise in productivity is seen in the wages in this sector which are, on average, about twice that of workers in other industries.

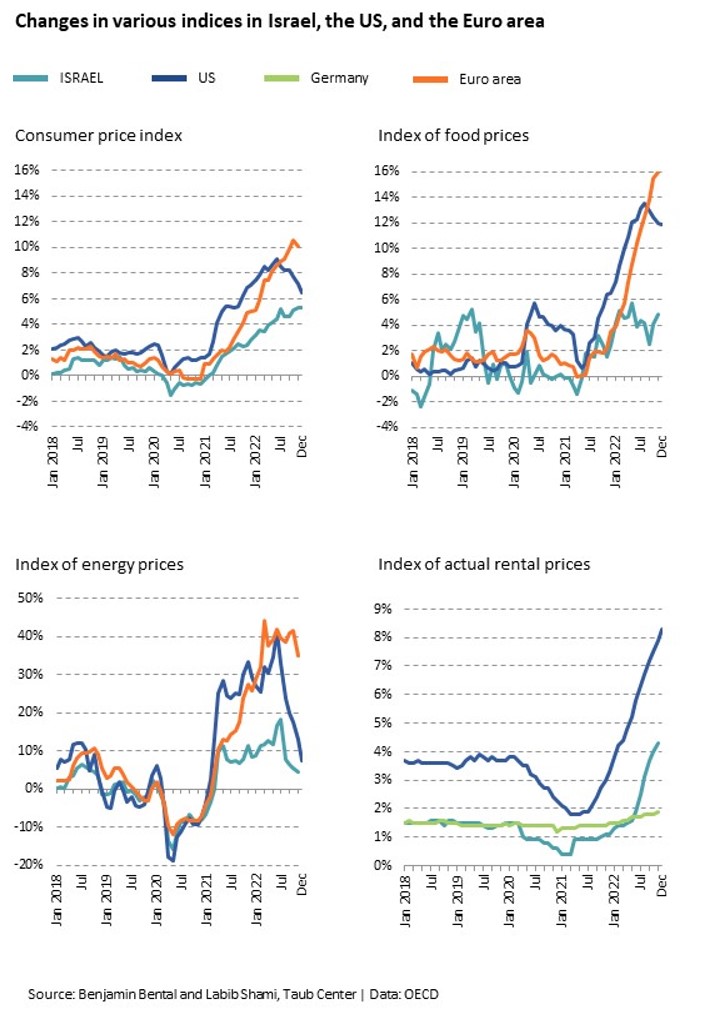

Price rises in Israel are far less than in the US or the Euro Area

In Europe and the US food prices rose more rapidly than the CPI, while in Israel, food prices and the CPI rose at about the same rate. The gap between Israel and comparable countries in energy prices is greater, though; in the US and Europe, energy prices rose by about 40%, while in Israel, the increase was about half of that rate.

With regard to the rate of price rises, the level of prices in Israel remains high relative to Euro Area countries and the US. The cost of living in Israel is tied to a great extent to the strengthening of the shekel, as well as to significant distortions in centralized markets like milk and other beverage products.

Price rises cause greatest harm to the weaker population sectors

Price rises do not impact all population groups in the same way, primarily due to differences in consumption patterns between population groups. For instance, households in the highest income quintile (where income per person is highest) spend more on home maintenance, health, transportation, and communication relative to households in the lowest income quintiles. In contrast, the situation with regard to home furnishings and equipment is the opposite: households in the lowest income quintile, spend about 3.6 times more than those in the highest quintile on kitchen appliance electrical repairs and about 30% more on plastic disposable dishes, which have become more expensive following their change in taxation level. Overall, following price rises, expenses for the average household in the lowest income quintile grew by about 10.2% relative to their gross income in 2019, while expenses for households in the highest quintile grew by only 4.6%.

In summary, despite the strong shake-up to the world economy due to COVID-19, the Israeli economy — as in other developed countries — recovered surprisingly quickly and has almost made-up the loss in GDP due to the crisis. Nevertheless, the researchers emphasize that there is work to be done to fix basic flaws that characterize the Israeli economy, among them, correcting the distortions in the incentive system in the private sector and the need for a substantial rise in public investment.

More research on this topic

A Picture of the Nation 2026: Israel’s Society and Economy in Figures

The Taub Center is publishing this year’s A Picture...

Avi Weiss

Public Capital and Economic Growth in Israel

Following the events of October 7, the Israeli economy...

Benjamin Bental Michael Debowy

Is the Israeli Economy Recovering?

State of the Nation Report 2025 – Chapter: Macroeconomic...

Benjamin Bental Labib Shami

The fiscal consequences of changing demographic composition: Aging and differential growth across Israel’s three major subpopulations

Among high-income countries, Israel has an unusual demographic profile....

Kyrill Shraberman Alex Weinreb