In 2018, employment is at an all-time high, unemployment is at a historic low, GDP growth is similar to recent years, and wages have risen. However, growth potential is declining due to demographic changes and trends in labor productivity, which is not growing at all.

Macroeconomic processes

The picture that emerges from an examination of developments in the major GDP components in recent years is one of stability and “balanced growth.”

- GDP growth for 2018 is expected to amount to 3.2% — slightly lower than in recent years, reflecting per capita growth of 1.2%.

- Since 2010, there have been no substantive changes in the relative shares of the main GDP components: private consumption, public consumption, fixed asset investment, exports and imports.

- Most of the volatility in fixed asset investment since 2010 is due to investment activity by the economic sectors: Between 2012 and 2015, the share of this kind of investment in GDP fell by 2 percentage points, but has risen by a little over 1 percentage point over the past two years.

- In terms of government consumption, the expenditure on the individual consumption component has shown stability over the years, while the collective component has fallen slightly (stemming from a decline in the share of security spending).Israel’s fiscal system is subject to growing pressure. In the 2019 budget, the government is deviating by 3 percentage points from the permissible amount, and it also seems to be on the verge of deviating from the legally specified deficit ceiling.

- Despite the deficit reduction of the last few years, Israel still has a larger deficit than most OECD countries. Israel’s national debt amounted to 75.6% of GDP in 2016 – a figure puts Israel near the middle of the OECD distribution.

- Assuming that the government will increase its expenditure in accordance with the relevant legal rules and limitations, it seems that as of 2020 the government will breach the deficit limit as it is set by law, and that the problem is likely to become even more severe in the long run.

- The budgetary problem is expected to increase further if the government follows through with its plan to increase the defense budget to about 6% of GDP, and peg it to the GDP growth-rate.

Growth and productivity in Israel

Israel is characterized by higher growth rates than those of other OECD countries. However, the same does not hold when examining growth per capita, and Israel’s productivity is not improving.

- In 2017, the Israeli economy grew by 3.5%, compared with an average OECD growth rate of 3.0%. However, because the Israeli population grew by 2% in 2017, the GDP per capita growth rate was only 1.5%, compared to 2.4%, on average, in the OECD.

- Israel is not managing to close the gap between itself and the OECD and G7 average (and the US) in terms of GDP per work hour. Israel’s GDP per work hour fell from 58% to 55.5% of the analogous US figure in 2016.

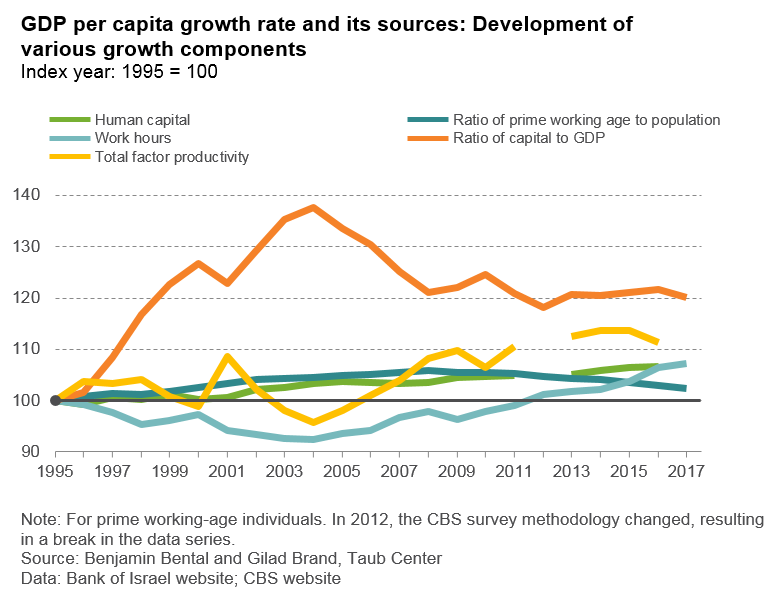

- Israel has experienced a slowdown in total factor productivity growth since 1973 (the rate of growth had been much faster between 1961 and 1973), and even the rapid growth experienced by Israel’s high tech sector from the 1990s on has not altered the slowdown.

- Since 2012, increasing employment has been the main source of Israel’s per capita GDP growth. Despite the fact that most of the workers joining the labor force were low-skilled workers, there was an improvement in the quality of employment due to an increase in experience and education levels. However, the working-age population is shrinking, as is the potential for future economic growth from increased employment rates.

Prices and the cost of living

The past few years have witnessed a sizable increase in real wages that is not attributable to improved labor productivity, but rather can be traced to a decline in consumer prices relative to the prices of all products and services produced in the economy. Nonetheless, prices in Israel remain high.

- Since 2015, wages have risen substantially, across all income levels and population groups.

- Expanded employment and the rise in wages were reflected in an impressive increase in households’ income and consumption. This was particularly apparent among households in the middle and lowest income quintiles (an increase of 16% and 13%, respectively, between 2012 and 2016), while among the highest income quintile there was a more moderate increase (9%).

- In recent years, prices in Israel have increased at a significantly lower rate than in the OECD. As a result, gaps between Israel and other developed countries have been narrowing and consumer prices relative to the OECD average have declined by 5.2% since 2014.

- The steepest price decrease among consumption categories was found for the communications category, with substantial price reductions for food, transportation, and recreation/ culture as well. At the same time, housing prices rose. It likely that the price decline also stems from measures taken by the government to lower the cost of living.

More research on this topic

A Picture of the Nation 2026: Israel’s Society and Economy in Figures

The Taub Center is publishing this year’s A Picture...

Avi Weiss

Public Capital and Economic Growth in Israel

Following the events of October 7, the Israeli economy...

Benjamin Bental Michael Debowy

Is the Israeli Economy Recovering?

State of the Nation Report 2025 – Chapter: Macroeconomic...

Benjamin Bental Labib Shami

The fiscal consequences of changing demographic composition: Aging and differential growth across Israel’s three major subpopulations

Among high-income countries, Israel has an unusual demographic profile....

Kyrill Shraberman Alex Weinreb