Author

The rising housing prices of the past decade have reduced the ability of the average Israeli household to purchase a home. However, when the ability to buy a home is assessed in terms of total disposable household income, rather than in terms of the number of monthly salaries needed to purchase housing (widely used in the media and public discourse), the findings show a more moderate decline in purchasing ability.

The reason for this is that total disposable household incomes rose more than wages did between 1998 and 2016, due mainly to a rise in the average number of income earners per household.

Measuring the ability to purchase a home

From the mid-1990s to 2007, many developed countries experienced housing price increases. Prices dropped somewhat in the wake of the 2008 financial crisis but, by 2017, have risen back to their pre-crisis levels. Since the second half of 2007, real housing prices in Israel have been trending upward (in annual terms). The consistency of this trend over the course of a decade, and the rate of increase, are unprecedented.

A households’ ability to buy housing is usually calculated in terms of the ratio between the average (or median) apartment price and the average (or median) individual wage – called the “average wage index” for the purposes of this study. However, this has many drawbacks as it does not take into account non-salary income or multiple household income earners. Thus, this study uses the “disposable household income index” to evaluate Israeli households’ housing-purchasing ability.

- Between 1998 and 2016, the average disposable income grew by 2.3% annually, while the average monthly wage increased by just 1%.

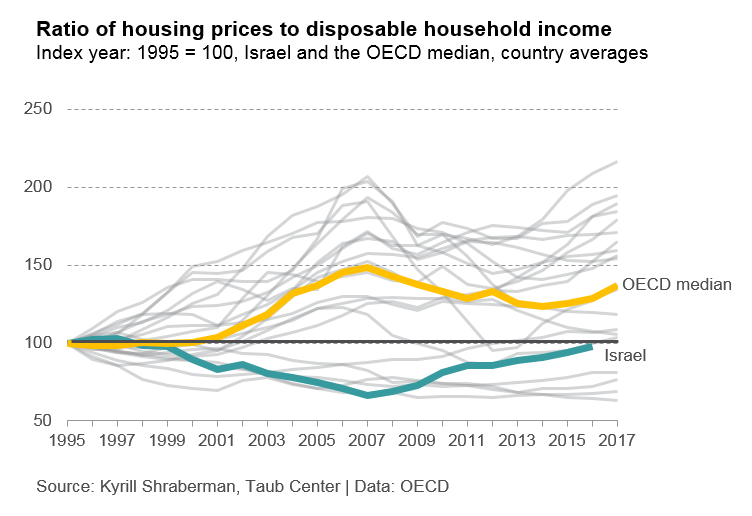

- Between 1998 and 2007/2008, both ratios declined – that is, the ability to buy housing improved. Since then, it has become harder to purchase housing.

- The ability of households to purchase housing in 2007 declined in most of the OECD countries relative to the end of 1990s. A similar picture emerged in Israel, but a decade later than in the other developed countries.

The ability to purchase housing by household characteristics

The figures described above provide a more general picture, but do not necessarily reflect changes in the ability to buy housing that occurred among specific population groups, or in different geographic regions.

- The disposable income of young adult households (25-34) grew at a rate similar to the average disposable household income between 1998 and 2016, so their ability to purchase housing was no more affected than was that of the general population.

- The age group whose housing-purchasing ability was most affected (the group whose disposable income rose at a lower rate than the general population) are households headed by individuals in the 35-54 age range, because the income of these households increased at a lower rate than the average for the general population.

- The ability to purchase housing has declined significantly in Tel Aviv, Jerusalem, and Israel’s Southern District. In the Northern, Sharon, and Gush Dan districts (excluding Tel Aviv), the ability to buy housing declined to a degree similar to the national average.

Housing Prices to Disposable Income Index ratio by locality

- Since 1998, the average disposable household income of immigrant families has risen at a faster rate than has the average Israeli disposable income: 2.9% between 1998 and 2016, versus an average annual change of 2.2% for native-born Israelis. This indicates that the ability of immigrants to purchase housing diminished to a more limited degree than the average for the public at large.

Household leveraging

A home is one of the largest purchases a household can make, and the vast majority of home buyers are obliged to take out loans in order to fund the purchase. As such, a useful indicator of households’ ability to buy housing is the credit available to them, and their ability to repay loans.

- The average level of household leveraging – the size of households’ net financial liabilities to creditors as a percentage of GDP – has increased since 2009, which could potentially make it hard for them to receive additional credit in the future.

- The following trends emerge when examining credit in terms of housing credit, non-housing credit, and net credit: the ratio between housing credit and GDP declined slightly between 2000 and 2007, then started climbing again and slowed around 2013; the ratio between non-housing credit and GDP increased from 10.1% in 2000 to 13.4% in 2009, halted between 2009 and 2013, then climbed until reaching 15.4% in 2017; the net credit to GDP ratio fell steeply from 27.1% of GDP in 2000 to 10.7% in 2009, then the trend reversed and the ratio rose continuously to reach 23.4% of GDP in 2017.

- The current level of leveraging is only slightly lower than it was in 2000, the year that witnessed the highest leveraging levels recorded.

The data show that rising housing prices have taken their toll on Israeli society. Since the second half of 2007, the ratio between housing prices and disposable income has increased, meaning that it was harder to buy housing in 2016 than it was in 2007.

Nonetheless, using the disposable household income index to measure this shows that the ability to buy housing did not decline as much as one might conclude if using the commonly-accepted average wage index.

More research on this topic

Housing Policy in Israel: Government Support for Different Housing Options

This paper is in Hebrew only. A lengthier, more...

Gilat Benchetrit

A roof over one’s head: the housing market in Israel

The high cost of housing and various proposals to...

Taub Center Staff