This chapter examines the activities of Israel’s welfare and social security systems over the past year, in the shadow of the October 7, 2023 massacre and the ensuing war. Prof. John Gal and Shavit Ben-Porat review changes in poverty rates and National Insurance Institute benefits, highlighting issues with the “Savings for Every Child” program and the food voucher program. They also detail the responses provided to those affected by the massacre and the war, as well as the ongoing challenges facing Israel’s welfare system.

Up to mid-November 2024, 1,785 Israeli civilians, foreign residents, and soldiers had been killed in the massacre and the war. The number of injured as of this date was 22,047 people. During the initial months of the war, about 143,000 residents left their homes in the Gaza border area and Northern border communities, with approximately 80,000 relocated to hotels and others to community settings. An estimated additional 120,000 evacuated independently. In the evacuated localities, the number of people using social services departments prior to the war was 32,000. According to the researchers, at least 17,750 of these individuals were evacuated from their homes.

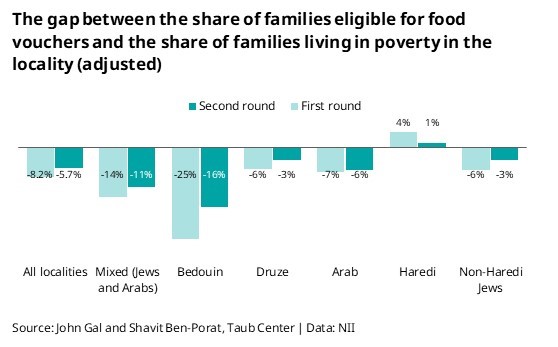

Changes in eligibility conditions for the food voucher program narrowed gaps, but challenges persist

Taub Center researchers have been monitoring the food voucher program since its launch in 2021 during the Covid-19 crisis. In a previous study, they examined the gap between the percentage of families receiving vouchers and poverty rates among families in each locality in the first distribution round of the program. The data and an analysis of the distribution of food vouchers in the second round and a comparison with the first round are presented here for the first time.

The comparison reveals that the average gap between the percentage of families eligible for food vouchers and the percentage of families living in poverty narrowed slightly, from 8.2% to 5.7%. However, the changes in the gap across different types of localities were uneven. In Arab localities, the gap narrowed the least, while in Bedouin localities, it decreased significantly (though these localities still show the largest gap). In Haredi localities — the only ones where a positive gap was found in the first distribution round — the gap also narrowed but remains the only positive gap.

Following the publication of these findings and additional critiques of the eligibility criteria for the program, it was decided about a month ago to modify its implementation.

Increase of NIS 41.5 billion in social expenditure, focused on social security and education

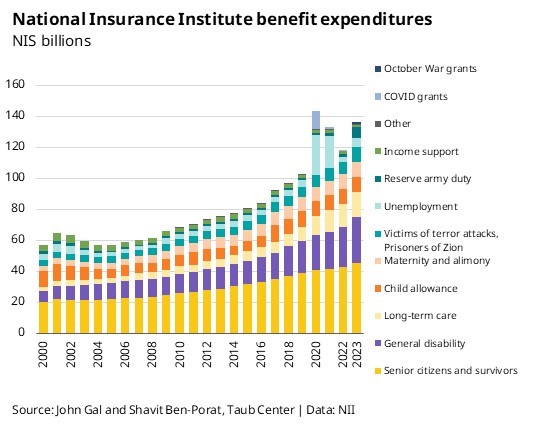

In 2023, social expenditure increased significantly. That year, approximately NIS 355 billion was allocated to social issues out of a total state budget of about NIS 564 billion. . Compared to the expenditure in 2022, This marks an increase of NIS 41.5 billion in nominal terms and about NIS 28.3 billion in real terms (2023 prices). The research shows that most of the increase in social expenditure — which includes spending on social security, healthcare, education, social welfare, and higher education — was concentrated in the areas of social security and education.

Social expenditure in Israel accounted for about 63% of total government expenditure in 2023, a slight decrease from the previous year, when it stood at 63.7%. Defense spending in 2023 constituted about 16% of total government expenditure, while other civilian expenditures accounted for approximately 21%, compared to 13.8% and 22.5%, respectively, in 2022.

Stability in poverty rates alongside an increase in national insurance institute benefits

Between 2020 and 2023, the poverty rate in Israel remained stable and exceptionally high, standing at about 20.7% of the population in 2023. Among senior citizens, there was a decline in the poverty rate in 2022, likely due to increased generosity in income support benefits for seniors whose primary income comes from National Insurance Institute allowances. However, the 2023 data indicate no change in their poverty rate. A look at poverty rates among families revealed a significant presence of self-employed family heads. It appears that the assistance provided to these families was insufficient to compensate for the substantial decline in their income, leading to an increase in their poverty rate.

There has been improvement in the effectiveness of National Insurance Institute benefits in addressing poverty, particularly due to increases in disability benefits and grants, as well as the easing of criteria at the onset of the war. However, Israel’s policies for poverty reduction remain especially ineffective compared to OECD countries. OECD comparative data on the number of work hours required for minimum-wage-earning families to rise above the poverty line reveal a significant disparity: in Israel, about 70 weekly work hours are required, compared to an average of 57 hours in OECD countries.

With regard to social security, in 2023, spending on National Insurance Institute benefits increased significantly, reaching approximately NIS 136 billion. This extraordinary increase was partly driven by war-related needs, including benefits for victims of hostilities, unemployment payments, reservist compensation, and grants for evacuees. Additionally, there was a notable increase in spending on general disability allowances. The researchers show that expenditure grew across all National Insurance benefits, except for income support allowances, which continued their downward trend.

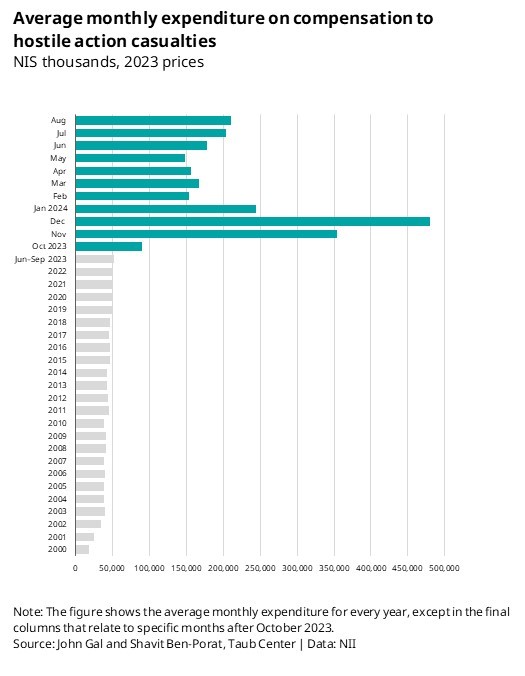

By the end of 2023, monthly spending on compensation for victims of hostilities had risen to approximately NIS 480 million, nearly ten times the average monthly expenditure in 2022 (in 2023 prices). This expenditure included initial grants and payments provided by the National Insurance Institute without supporting documentation under an expedited process for recognizing victims of hostilities. These payments included two medical treatment allowances granted based on family composition and age (the first ranging from NIS 2,883 to NIS 5,977 and the second from NIS 3,460 to NIS 8,972). Additionally, a one-time organization grant of NIS 3,500 and an advance payment of NIS 1,500 against medical treatment compensation were provided. As of September 2024, there were 16,545 recognized victims of hostilities, compared to an average of about 5,000 annually in the decade preceding October 7, 2023.

With the outbreak of the war, the number of unemployment benefit recipients surged, reaching approximately 206,000 in November 2023. The labor market then gradually began returning to full activity, and by June 2024, the number had nearly reverted to pre-war levels. This increase led to a rise in National Insurance Institute spending, adding approximately NIS 2 billion in expenditures during the first six months of the war.

Changes were made to the “Savings for Every Child” Program, but they have not fully achieved the goals

In July 2024, two significant changes were made to the “Savings for Every Child” Program. The first change established a new default for depositing savings for children whose parents had not chosen an investment track: funds will now be deposited into a provident fund with a higher-risk investment profile, expected to yield higher returns over the long term. The second change introduced the option to transfer savings managed in a bank to a provident fund — an option that was not previously available.

A recent report by the National Insurance Institute on the program indicates that in 2023, approximately 21% of savings plans were managed in banks, with the rest in provident funds. Furthermore, at least one-third of the plans were placed into a default investment track due to a lack of active parental choice.

These changes are expected to affect vulnerable populations in particular. Analysis of program data for 2018–2019 reveals significant disparities among parents from different demographic groups, both in their involvement in selecting an investment track and in the chosen track itself. The analysis found that the higher the parents’ income quintile, the more likely they were to actively select an investment track. Additionally, the program allows parents to double the monthly savings by adding an amount equal to the government’s deposit from their child allowance. However, the analysis shows that only about 22% of parents in the lowest income quintile made this additional deposit, compared to about 65% in the highest quintile. The program’s failure to address this disparity undermines one of its central goals: reducing inequality.