Individual chapters are available here, or by clicking the chapter’s name.

The State of the Nation Report 2021, part of the Taub Center’s Herbert M. Singer Series, offers new data and in-depth analyses of the past year’s developments in the economic, labor market, social welfare, healthcare, education, and demography spheres. The report includes eight new chapters that deal with the budgets of government ministries and with their use of additional budgets for the Covid-19 crisis, the recovery of the economy following the crisis, the challenges in dealing with it, and a look forward to what to expect. From the Taub Center data it appears that the Israeli economy recovered rather rapidly, though the labor market has not completely recovered and there is an apparent fall in the labor force participation of Arab men and, to a lesser extent, Haredim (ultra-Orthodox Jews), as well as a disappointing amount of vocational training. In a look at returns to education and experience in the labor market, it appears that returns are still influenced by sector (salaries in the Jewish sector rise more than among Arabs), and with respect to experience, the greatest returns are acquired by Ashkenazi Jews. From a demographic perspective, there is a small rise in mortality and fall in life expectancy, alongside an increase in fertility rates among Jews in Israel – as opposed to other developed countries. Israel lags behind other countries in dealing with certain diseases including diabetes and specific types of cancer, and there are several areas worthy of investment by the healthcare system to narrow health inequalities among Israeli populations. From the health workforce perspective, although the number of healthcare workers has increased, there remains a shortage in view of the rapid population growth. In welfare terms, the policies of the current government will improve the circumstances of certain population groups (like the elderly), but it will not help those living in poverty, or those who are in need but have difficulty in taking up their rights.

The editor of the Report is Prof. Avi Weiss, President of the Taub Center and Professor of Economics at Bar-Ilan University.

Macroeconomic Trends: The Precipitous Downturn and Rapid Recovery of the Israeli Economy

Prof. Benjamin Bental and Dr. Labib Shami

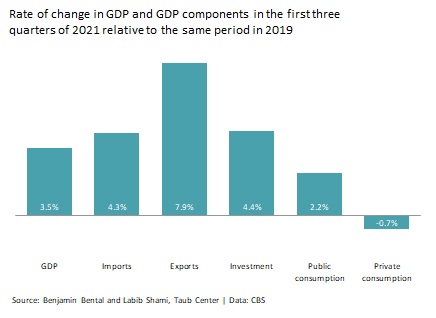

Israel’s economic recovery was more rapid than anticipated by the Bank of Israel, the International Monetary Fund, and the OECD. Due to the Covid-19 pandemic, the Israeli economy lost about 6% of its GDP in 2020, compared with what would have been expected for that year had the crisis not occurred. Private consumption fell dramatically by around 13% versus the growth that would have occurred without the pandemic (nearly double the decline in countries that suffered a similar drop in GDP), while public consumption increased in 2020 at a rate similar to that of the previous year. Israel was also unusual in that its balance of trade improved substantially due to a steep decrease in imports. The growth in public consumption, along with the sharp drop in imports, moderated the percentage of GDP decline.

The exceptional drop in private consumption may have resulted from the harsh preventive measures taken by the Israeli government, and was also evident in an approximately 4% increase in gross private disposable income. Gross private savings rose by about 8.5% of national income, evidently due to forced savings arising from restrictions on the consumption of services in the high-proximity sectors (sectors with high potential of contagion due to physical proximity). A sharp drop in consumer confidence may also partly explain the increase in private savings. Google’s mobility index for retail trade and leisure activities shows an average decline of 34% in the physical presence of consumers at commercial and recreational sites in 2020. This percentage is high compared with other countries, and is yet another indication that the impact of the pandemic and the closures was stronger in Israel. However, Israel’s decline in GDP per capita in 2020 was 5.7%, close to the OECD average. Per OECD assessments, Israel was expected to return to its Q4 2019 GDP per capita level only in early 2022, but the country recovered much faster, and GDP returned to that level by Q2 2021.

Government revenue is high, but so is the deficit: A look at government revenue, expenditure and budget surplus for the years 2020-2021 versus 2019 points to a dramatic increase in the deficit at the beginning of 2020, but the economy’s swift recovery led to revenue growth, such that revenues were even higher in early 2021 than they were in 2019. Government expenditures declined with the drop in morbidity and progress on the vaccination campaign, so the deficit dropped. After three quarters of 2021 the deficit amounted to 4.6% (versus 3.7% in 2019).

The budget earmarked for improved distance learning and for vocational training is not being sufficiently utilized: The total expenditure framework for pandemic-related economic relief in 2021 and in the coming years is NIS 82 billion. As of late September 2021, the budget implementation rate stood, on average, at 88%: 96% implementation for social security, 83% for healthcare and civil services, 85% for business continuity, and only 61% for acceleration and development of the economy. Particularly low implementation rates, capable of disrupting Israel’s economic recovery and return to a growth trajectory, were found for supplier credit insurance and additional credit, and for deferral/discounts on business licensing fees (0%), refunding of prepayments via the Tax Authority (2%), an accelerated depreciation benefit (35%), encouragement of high-tech investment by institutional entities (44%), digitization, including remote learning (42%), and vocational training programs (41%). For some items, such as vocational training, the under-implementation of budgeted expenditures may stem from conflicts of authority between government ministries, and from delayed release of the budget.

The Israeli economy can tolerate a temporary increase in the deficit and in the debt to GDP ratio: The nominal interest on Israeli debt ten years from now stood, on average, at slightly less than 1%. At a nominal growth rate of 4.9% per year, such an interest rate allows Israel to maintain an initial deficit of 2.2% and to return in the long term to a debt-to-GDP ratio of 60%, which will bring the fiscal deficit to a level of 2.8% of GDP. In terms of savings, the global markets do not seem to fear Israeli economic collapse. The markets assess the risk of Israeli state insolvency at one percent per year – a historic low as witnessed by a 40 basis point premium on Credit Default Swap (CDS) deals.

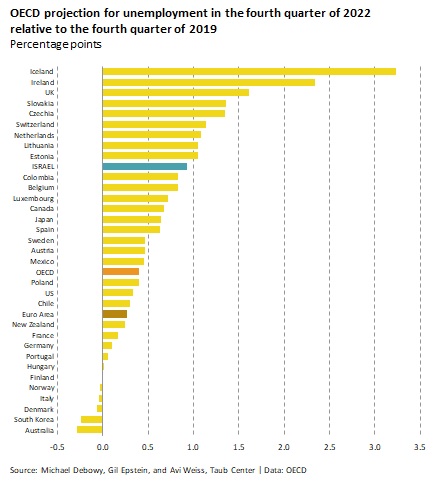

The labor market is recovering, but not enough: Per OECD assessments, Israel’s labor market was expected to return to its 2019 activity level only in early 2025, but here as well the data indicate a much speedier recovery. The vaccination campaign’s impact is particularly evident in this recovery, but 65,000 workers (0.8% of the labor force) who left the labor market due to the Covid-19 crisis have yet to return to it. Likewise, compared with the state of the market before the pandemic, there are an additional 100,000 unemployed persons, apparently from the entertainment, tourism, and leisure sectors, which were hit especially hard by the pandemic.

The Israeli Labor Market in the Wake of COVID-19

Michael Debowy, Prof. Gil Epstein, and Prof. Avi Weiss

Israeli workers bore a large portion of the burden of the Covid-19 crisis, more than did their counterparts in the OECD: In order to deal with the collapse of employment during the Covid-19 pandemic, some nations adopted the “German model” in which the state partially subsidizes work hours and even provides partial wage subsidies for workers whose hours have been cut, so as to maintain the employer-employee relationship and work routine. Israel adopted the furlough model that allowed workers who completely ceased working to collect unemployment insurance, but did not help workers who experienced work hour reductions. The Israeli choice resulted in workers bearing 45% of the cost burden of the work hour reductions, compared with 24% on average in countries that employed the German model. Israeli employers did not have to bear any part of the burden, while OECD employers bore, on average, 7%-9% of the cost. In Israel the state bore 55% of the cost (via unemployment insurance), versus 65% on average for the OECD countries. In other words, Israel placed a larger share of the burden on workers, and a lesser share on employers and on the state.

In terms of work hours, the average reduction in the OECD was 7.5% – and even less in countries that adopted the German model – while Israel lost over 9% of its work hours relative to late 2019. Should additional lockdowns be required in the future, adopting the German model could benefit Israel’s labor market.

Labor market polarization increased: During the crisis, the number of workers in most economic sectors declined, with disproportional declines in tourism and food services. In white-collar sectors (such as management and support services, real estate, and communications) there were almost no work hour reductions. Healthcare, social services, and welfare services – sectors heavily engaged in addressing the crisis – actually displayed job growth, as did other “public” sectors such as local and public administration and infrastructure supply. However, some of the employment decline in certain sectors might have occurred even without the crisis, due to deep-rooted processes already underway in the economy.

When we look at work hours per worker figures from early 2020 to mid-2021 relative to 2019, we find that the average number of weekly work hours per worker rose in almost all economic sectors. In the public sectors there was a per-worker work hour increase in addition to a rise in employment – evidence of a growing volume of activity in these sectors. Despite the extensive damage suffered by the trade, tourism, and food service sectors, Q2 2021 showed an impressive comeback in per-worker work hours, nearly to pre-Covid-19 levels, though job numbers remained tens of percentage points lower.

In Israel, as in many other countries, polarization in the labor market worsened during the crisis and the ongoing recovery period. While high-wage sectors such as high-tech and public services experienced minimal damage and recovered quickly, low-wage and low-human-capital sectors (such as agriculture, tourism and food services) suffered major damage and their recovery has lagged behind the rest of the economy. Workers in the labor market’s middle layer (sectors such as manufacturing, construction, and trade) sustained a harsh blow and are having trouble recovering, even where the sectors themselves recovered. As a result, assisting workers who were harmed will require adopting a differential policy.

A drop in employment among Haredi and Arab Israeli men: When we look at employment rates in the 25-64 age range by gender and population group, we find that in the Haredi sector women’s employment rates remained stable and actually rose. Regarding men’s employment, a decline was found among Haredim, and an even larger drop in the Arab Israeli sector. Arab Israeli men’s employment rates had started to fall well before the crisis, apparently due to a lack of appropriate skills, low human capital, the replacement of Israeli construction workers (most of them from the Arab Israeli sector) by foreign workers, and demographic growth among young Arab Israelis under the age of 35 without a parallel increase in demand. We would note that in the third quarter of 2021 there is an expected reversal of the trend with an increase in employment rates for Arab men and women

Adjustment to working from home: In all of the “tangible” production and service sectors that require physical presence (such as manufacturing, transportation, retail, and construction), work from home rates were low, while the “intangible” sectors (e.g., information and communication, real estate, and financial services) displayed an opposite reality – work from home rates were higher than average for the economy as a whole. During the course of the year, the decline in online work hours was very slow, apparently reflecting adjustment to a new reality in which working from home plays a central role, even without the pandemic. Major fluctuations in the volume of remote work were found, as expected, in the education sector, and, contrary to expectations, in the energy and air conditioning sector. The scope of remote work was very high among those in occupations requiring academic training, but was lower among managers, practical engineers and clerical workers, and low among production, sales, and service workers.

Student numbers rose: In the absence of employment options or the ability to travel abroad for extended periods during the pandemic, Israel experienced the well-known phenomenon of young people’s increased enrollment in institutions of higher education. The surge in bachelor’s and master’s degree enrollment numbers was more than 15 and 14 percentage points (respectively) higher than the average annual increase for the previous eight years, with the largest increase among those in the 20-24 and 27-28 age groups. In terms of study concentrations, sharp upturns were observed in the percentage of women enrolling for study in the biological sciences (an increase of 37%), business (28%), and engineering (18%), and in the share of men enrolling for study in business (an increase of 22%), the social sciences (21%), and the biological sciences (19%). The most modest enrollment rate increases were in education studies among women (9%) and mathematics, statistics, and computer science studies among men (9%).

Disappointing vocational training participant numbers: Despite the surge in unemployment, the number of those participating in Israeli Employment Service vocational training programs declined during 2020 by 35%, chiefly during the lockdowns. Although some training programs can be offered online, this seems to have been hard to arrange, given the substandard Internet infrastructures available to those in greatest need of such programs (in Israel’s geographic periphery and in the Arab Israeli sector). Many unemployed persons likely refrained from utilizing the training programs because they expected a speedy return to work. As the population became vaccinated and the lockdowns were cancelled during 2021, the placement and vocational training activities came back in full force. Because unemployment rates have remained relatively high, the demand for these activities has likely remained high as well. Nevertheless, because a large majority of workers have indeed gone back to work, fewer people are likely to benefit from the training programs than could have benefited during and between the lockdowns in 2020.

Returns to Education and Experience in the Israeli Labor Market

Michael Debowy, Prof. Gil Epstein, Prof. Avi Weiss

Since 2003, labor market participation rates have been on the rise, particularly among Arab Israelis, Haredim, and women. The increase likely stems from social benefit cutbacks that pushed many people into the labor market. At the same time, the share of those eligible for a matriculation certificate has grown since the early 2000s from less than 50% to 70%, the number of bachelor’s degree students has climbed by 50%, and the number of advanced-degree students has grown by 80%. Within the Arab Israeli population the changes have been even more pronounced: between 2005 and 2017 the number of Arab Israelis pursuing bachelor’s degree studies increased threefold, and the number studying for advanced degrees increased fourfold. Taub Center researchers looked at the degree to which these developments had an impact on economic returns to education and experience for male and female workers in Israel.

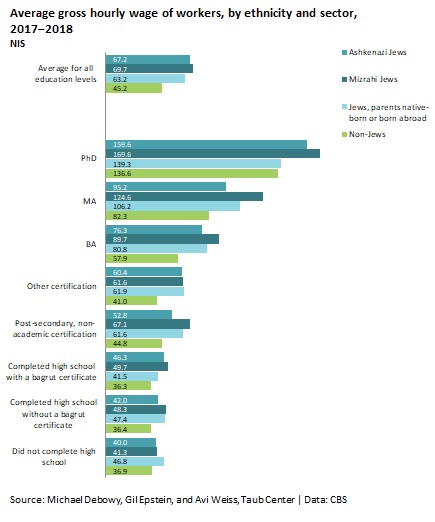

The researchers used data on the 17-67 age range from Central Bureau of Statistics household expenditure and income surveys for the years 2017-2018, while distinguishing between Jews and non-Jews and between Jews of different ethnic backgrounds. The findings show that employment rates rise with education level: for those who did not complete high school, employment rates are below 40%; for high school graduates the figure is 70%, and for academic degree holders – over 80%. The highest employment rates belong to doctoral degree holders, nearly 90% of whom are employed. Earnings also increase as education levels rise, but the average wage of matriculation certificate holders is not higher than that of high school graduates without a matriculation certificate – i.e., the matriculation certificate has little added value unless it is accompanied by further study.

Sector has a substantial impact on earnings: At all education levels, Jewish workers earn more than do non-Jewish workers, but at most education levels no differences were found between Ashkenazi and Mizrahi Jews. Nonetheless, education level has an effect on earnings, and the study found that the percentage of Arab Israeli workers who did not finish high school is nearly double that of Mizrahi Jews, while the share of Mizrahi Jews who did not complete high school is double that of non-Mizrahi Jews. Earnings are also affected by occupation and employment sector; variance in the share of academic degree holders explains 60% of the average hourly wage variance between different occupations.

Academic degree holders enjoy considerably higher returns: A multi-factor analysis encompassing gender, family status, and geographic location supports what was expected – high school graduation increases the probability of employment by 46%, a matriculation certificate raises it by 61%, a vocational degree by 69%, a bachelor’s degree by 78%, a master’s degree by 84%, and a doctoral degree by 92%. Women work less than men, and Ashkenazim less than non-Ashkenazi Jews. When the impact of education on hourly wage was examined, it was found that it increases with each additional degree. After controlling for other variables, it was found that each additional degree raises the wage, but less than it appeared from simple averages. Compared with those who did not complete high school, high school graduates without the matriculation certificate enjoy only a 12% higher hourly wage, while those with vocational degrees earn 26% more, bachelor’s degree holders earn 45% more, master’s degree holders 61% more, and doctoral degree holders 90% more.

Experience also has a strong effect on earnings. Academic degree holders reach their peak wage within a shorter timespan than others – the positive return to each additional year of experience peaks after 24 years, versus 31 years for the general population. This figure may reflect later career starts after many years of schooling, or depreciation of the human capital acquired in academia.

The returns to education for bachelor’s degree holders has not changed: Taub Center researchers have also found that the return on high school education declined over the years, reaching stability within the past decade, while the return on a bachelor’s degree remained unchanged, and the returns on master’s and doctoral degrees grew considerably. The findings point to a phenomenon of “education inflation,” in which degrees lose their comparative advantage as more people in the labor market acquire them. In terms of gender, men and women may be expected to enjoy similar returns at different levels of education, but women’s monthly wages are, on average, lower than those of men.

Ashkenazim enjoy the highest returns on experience: When ethnic and sectoral gaps were examined, no significant differences were found in returns on education. Non-Jews’ wage levels were substantially lower than those of Jews, that is, the sectoral gap remains at all education levels. Regarding experience-driven wage increases, there is a major difference: while Jews of mixed sectoral background and third-generation Israeli Jews enjoy higher earnings that extend over a 30-year period and peak at a 76% increase over their entry-level wage, Mizrachi workers need 36 years to reach a peak increase of 78%, while Ashkenazim need 37 years – though they reap a return of 105%. Although the work experience of non-Jews reaches peak return after a shorter period – 25 years – their maximum wage increase is only 25%. Statistically significant differences between women and men were not found in any group.

The Taub Center research indicates that, overall, the path to employment and to occupations that make optimal use of worker skills is that of formal higher education. In light of education’s positive effects, and the barriers (economic, geographic, and other) that make it difficult for various populations to pursue higher education, ways must be found to support disadvantaged groups. Solutions should focus on economic and geographic accessibility, e.g., furthering access to education in the periphery by opening new institutions, promoting online study and improving the infrastructures relevant to it – while also addressing language and cultural difficulties.

The Israeli Education System: Its Demographic Composition, Manpower, and Budget

Nachum Blass

The share of students in Arab Israeli education is declining, while the share in Jewish education is stabilizing: Over the past decade, the share of students in State-Jewish, State-religious, and Haredi education has stabilized, while that of Arab Israeli education has declined. The stabilization of the share of students in State-Jewish education can be explained by rising fertility rates among secular women, secularization processes driving pupil migration toward less-religious education streams, and an increase in the number of non-Jewish pupils in Israel’s State-Jewish educational frameworks. In the Arab Israeli sector there have been particularly large-scale changes, with the share of pupils in grades 1-4 out of all pupils in that age group dropping from 28% in 2010 to 22% in 2020. A rise in the share of pupils in Arab Israeli high schools can be attributed mainly to lower dropout rates.

Special allocation for Covid-19: In 2020 the Ministry of Education’s actual budget amounted to NIS 67 billion, NIS 64 billion of which was utilized. In order to contend with the Covid pandemic, a sum of NIS 4.2 billion was allocated in the 2020/2021 school year (NIS 1.75 billion in 2020 and NIS 2.45 billion in 2021), to improve infrastructures for remote and hybrid learning, for protective/hygienic measures, and for assistance to special populations. Of this 2020 allocation, the majority of the additional budget was spent on afterschool programs (NIS 870 million) and on equipment and the training of teachers for afterschool programs (NIS 280 million). Only NIS 400 million were spent on additional teaching staff to operate the class-size-reducing “capsule” system. All told in 2020, NIS 1.7 billion shekels of the 2020/2021 budgetary addition was spent. It is surprising to find that a relatively small amount of the allocation was actually used to split classes.

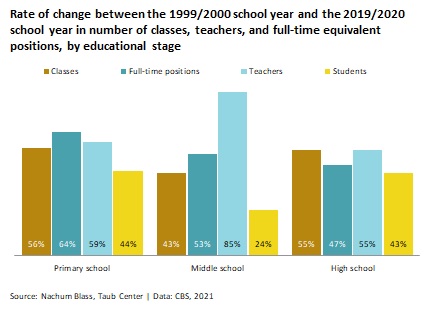

Reducing class sizes, increasing the number of teachers: Over the past twenty years, the Ofek Hadash and Oz LeTmura labor agreements were signed with Israel’s teacher organizations, implementation of the Compulsory Education Law was extended to age three, and special education frameworks grew in number. All of these things affected the number of teachers, pupils, and classes, though there was notably a more rapid rise in the number of teachers than in the number of pupils and classes.

Class sizes in the State and State-religious education streams decreased, as they did to an even greater extent in the Arab Israeli education stream – a development that reflects a narrowing of gaps due to policy and changing trends in Arab Israeli family size. By contrast, class sizes increased in the Haredi education stream – apparently reflecting the Haredi population’s numerical growth.

Regarding teachers, while the share of female Jewish teachers among all Jewish teachers has not changed over the past two decades, the share of female teachers in the Arab Israeli sector grew from 60% to 70%. The teachers’ education level rose, especially in the Arab Israeli sector: from 47% without a degree in 2000 to just 3% in 2020 (less than the percentage in the Jewish sector). The share of Arab Israeli teachers with master’s degrees is similar to that of their Jewish counterparts – 38%. There was also an increase in work hours, apparently due to job structure changes following agreements with the teacher organizations, e.g., additional one-on-one hours and hours not formerly included in the work hour calculation (though they were in fact hours in which teachers had worked). There was, however, no change in the scope of employment for individual teachers (i.e., percent of full-time equivalent) and most teachers work part-time. In terms of qualification for the field, the percentage of teachers with the training required for math, English, and Hebrew instruction has not been on the rise and at times has decreased; the lack of qualification is evident primarily in the Jewish education stream.

In order to examine Israel’s teacher shortage, several parameters need to be examined, such as whether there has been a rise in the average job position (how many hours teachers work on average), an increase in the number of unlicensed teachers and decline in the level of education required, a rise in the number of students per class, a fall in the number of teacher hours per student, a decrease in the number of learning hours per subject, and the disappearance of certain study majors. Since 2010 there has been a decline in the share of non-certified teachers, from 16% to 6%, while the number of teachers with master’s degrees has risen from 24% to 38% – indicating that the level of instruction has improved. The average number of pupils per class is dropping, and the number of work hours per class is rising – a situation that does not point to a teacher shortage. In terms of teacher training institution graduates’ entry into the field, only 60% went on to work in teaching during the period 2000-2017, meaning that there is a potential pool of 40% who could be recruited for work in the system during crisis periods. Additionally, the share of new teachers exceeds that of retiring teachers; here as well there is no indication of a shortage.

Nevertheless, there are always point-specific teacher shortages in certain subject areas, and Taub Center Researcher Nachum Blass proposes several means of addressing the problem: generous overtime compensation, paying retired teachers to reenter the system with no sacrifice in terms of their pensions, and maintaining a “teacher roster” to facilitate contact with teacher certification holders as needed.

The Health Workforce in Israel During the Covid-19 Pandemic: An Overview

Prof. Nadav Davidovitch, Dr. Baruch Levi, Rachel Arazi

At the end of 2020, there were 32,000 physicians in Israel, an increase over the previous year. This figure included 8,300 residents. However, the supply of medical personnel relative to population size is actually declining, due to the rapid growth of the population coupled with physician ageing and retirement, and there is also an evident shortage in certain medical specialties. Physicians report excessive workloads, tend to work in more than one framework, and combine work in the public and private healthcare systems.

Physician and nursing staff numbers declining relative to population growth: The past decade has witnessed a steep rise in the number of new physicians per year, but despite a 26% numerical increase, there are fewer physicians per thousand people, due to the rapid rate of Israeli population growth. Moreover, Israel’s share of medical school graduates is among the OECD’s lowest, and Israel has the highest percentage of graduates of foreign medical schools. There are disparities in the quality of training between medical schools in Israel and in other countries, for instance in medical licensing exam pass rates. In an attempt to address these gaps, the Ministry of Health has shortened the list of foreign medical schools recognized in Israel. With regard to nursing staff, the numbers are again lower than in the OECD, with a gradual increase in the ratio of registered nurses (about 5.7 per 1,000 population) and a decrease in the ratio of practical nurses, with 0.7 practical nurses per thousand people in 2020.

When we look at physicians by gender and age, we find that Israel has one of the highest shares of older physicians among developed nations – half of the country’s doctors are aged 55 and over. During the coming decade, a third of the Israel’s veteran physicians are expected to retire. The share of women physicians has been trending upward, and this has an impact in a number of areas. Female physicians tend to work fewer hours than their male counterparts, such that the overall supply of physician work hours will decrease. There are also implications for choice of specialty. In addition, with the overall increase in the share of women physicians, it is expected that their representation in managerial positions will also increase.

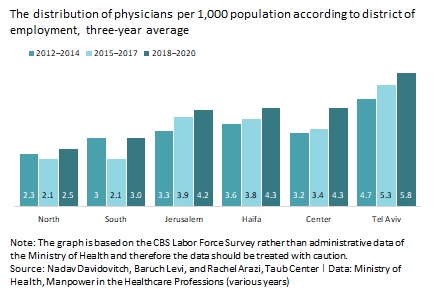

Healthcare infrastructure disparities between districts and population groups: The hospital bed to population ratios in northern and southern Israel are the lowest of all the country’s districts, and there are disparities in terms of geriatric rehabilitation and general rehabilitation beds, as well as in the distribution of infrastructures and medical personnel. The Tel Aviv District’s physician to population ratio is the highest – twice as high as that of the Northern District. There are also medical specialties that are insufficiently accessible in the periphery, forcing patients to travel long distances. It appears, however, that in specialties with relatively low levels of demand, healthcare service decentralization would be infeasible, both medically and economically, and that it would be better to invest greater resources in fewer major centers than in wider service distribution while at the same time investing in transportation development, dedicated transportation for patients, and the development of community-based primary medical services.

Another way to improve access to healthcare services is to create new roles for non-physician health personnel such as practice nurses authorized to diagnose patients and prescribe medications, pharmacists authorized to prescribe prescription drugs, and a new profession that has emerged in recent years – the physician’s assistant, who provides preventive/diagnostic services and treatment under physician supervision. The continued development of this profession may be expected to significantly ease the shortage of medical personnel.

The poor are less immunized against Covid-19: Rates of immunization against Covid-19 rise along with socioeconomic status for all age ranges over 20. Vaccination gaps are evident in the lower socioeconomic clusters, not just in terms of delaying the third dose but also in refusing it altogether. That is, Israel’s socioeconomic disparities are also manifesting in the pandemic’s impact on the population at large, and their impact may be expected to persist, given the disease’s long-term physical, mental, and socioeconomic effects.

The Social Welfare System in Transition

Prof. John Gal and Shavit Madhala

In 2020, Israeli social expenditure grew by NIS 55 billion, mainly due to the need to address the Covid-19 pandemic. 69% of the increase resulted from greater social welfare spending (social security and social services), mostly spent on increased expenditures on unemployment benefits and the universal grants that were disbursed. There was no substantive change in social welfare (social services) expenditure, with growth of only 4.5%, lower than the 2019 increase. The distribution between the social spending components – social security, social welfare, healthcare, and education – remained similar to that of earlier years. Most of the resources allocated to social welfare in the pandemic relief plan were devoted to social protection programs for those who lost income due to the crisis, with only a small portion allocated to social investment programs aimed at developing human capital and adapting workers to the labor market.

Israeli governmental policy will benefit people with disabilities and senior citizens, but may make things worse for those living in poverty: The directions in which social security has been developing seem contradictory; on the one hand, the government plans to continue with measures that were underway before the crisis and that aim to improve the way in which the needs of senior citizens and people with disabilities are addressed. These measures include implementation of the agreement with the organizations for people with disabilities (an agreement to improve and expand the general disability allowances), and increasing the income supplement for senior citizens who have no other sources of income. On the other hand, planned policy for families with children could potentially worsen their status and raise the incidence of poverty among this population, due to stiffened eligibility criteria in the unemployment insurance program, and a failure to address limitations within the income support program.

The labor market’s return to proper functioning in the second half of 2021 made it necessary to adjust the unemployment insurance program to the new reality, and to strike a new balance between protecting the jobless and encouraging unemployment recipients to return to the labor market. The adjustments include unemployment benefit reductions for vocational training program participants, returning the qualification period to its pre-pandemic length, and cancelling the entitlement period extension for ages 45 and over. The measures that took effect in mid-2021 had an immediate impact, reducing the number of unemployment recipients to 156,000. The expansion of unemployment insurance coverage during the pandemic provided an alternative safety net to most of those hurt economically by the crisis; as a result, the number of income support recipients grew relatively little during this period. However, given the stiffening of eligibility criteria for unemployment insurance and the difficulty that many experienced in returning to the labor market, an increase in the demand for income support is anticipated. Another assistance program is the Work Grant program operated by the Israel Tax Authority. Although modifications have been made to the program over time that have enlarged the pool of those eligible for it and improved its accessibility, its less-than-generous offerings undermine its effectiveness as an anti-poverty measure, and it suffers from low uptake, with 30% of eligible recipients not utilizing the program.

At the same time, after extended public debate, it was decided to take a major step to strengthen the National Insurance Institute’s financial robustness, in the form of raising the retirement age for women (i.e., deferring the age of entitlement to the old age pension). This measure will be accompanied by steps to ease the economic harm suffered by women on the verge of retirement – such as lengthening the eligibility period for unemployment benefits, increasing the income supplement and making it possible to receive it at higher wage levels, offering an adjustment grant, and increasing the amount of the work grant for women ages 60 and over.

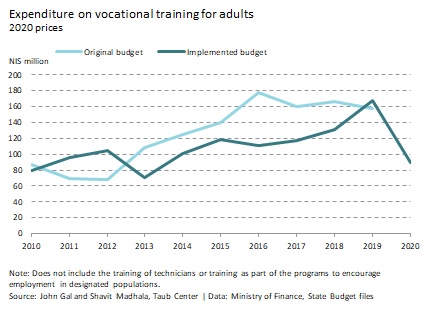

Despite the great importance of vocational training, especially at a time when many unemployed persons lack higher education, it was evidently very hard to advance such training and to utilize the funds that were allocated for it. As part of the pandemic relief plan, the government allocated NIS 1.4 billion for vocational training and for the Council for Higher Education, but only a third of that allocation was actually utilized. Moreover, expenditures on vocational training for older people in the Ministry of Economy and Industry’s Labor Branch’s ongoing budget declined substantially in 2020, while the number of participants in training programs funded or subsidized by the Ministry’s Training Division also dropped, with a total that year of only 7,000 participants. Investment was also curtailed in training programs to encourage employment among specific populations (Haredim, Arab Israelis, single parents).

Disadvantaged populations have trouble exercising their rights: When we look at the degree to which rights are exercised among eligible populations, we find 99% utilization of the child allowance and the old age pension, but low utilization rates for programs where the receipt of benefits is means-tested or requires navigation of complicated bureaucracy. Uptake rates stand at 75%-79% for the disability pension, 70% for the work grant, 48%-63% for income support, and only 32%-40% for unemployment insurance such that a large proportion of the populations that need social security benefits are not exercising their right to assistance. This non-utilization generally stems from lack of awareness, or from reluctance to deal with bureaucracy. It is clear, however, that factors related to the structure of the programs, such as income tests, complex entitlement criteria, accessibility barriers, and bureaucracy, have an impact as well. The National Insurance Institute and civil organizations have taken steps to increase the utilization of entitlements, but as yet it is hard to assess the degree to which these measures are succeeding.

No progress on implementation of the recommendations of the Committee for the War Against Poverty (the Elalouf Committee): Since the government adopted the recommendations of the Committee for the War Against Poverty (the Elalouf Committee) in 2014, the Taub Center has been tracking their implementation. In 2020 progress was made solely in the sphere of education, while there was no progress, and in fact reduced investment, in housing, employment, and economic areas. With regard to social welfare and social security, investment remained generally the same, amounting to a third of the addition recommended by the Committee. Moreover, the recommendation to enlarge the income support budget for working age people living in poverty has yet to be implemented, though a decision was made in summer 2021 to increase the income supplement for the elderly, which is expected to raise Israel’s social welfare expenditure next year.

Prof. Alex Weinreb

A rise in mortality rates and a drop in life expectancy: The Covid-19 pandemic has driven mortality levels significantly upward: 60% of Covid-19 deaths in Israel occurred in 2021. The new variants (at least until Omicron) have raised the case fatality rate for the disease among younger people, which will push life expectancy in 2021 down to 2016-2017 levels. It does not appear that there will be a return to pre-pandemic mortality patterns while vaccination rates worldwide remain low, since the absence of vaccination allows more variants to emerge and spread across the globe, with a continuing impact on mortality and life expectancy.

Israeli fertility rates are higher than those of other developed nations, but the patterns are changing: Between 2018 and 2020, even before the pandemic hit, Israeli fertility rates fell sharply in all sectors. In 2020, the fertility rate for Jewish women was 3.0 children per woman, while for Christian women the rate was 1.83 – a decline of 0.2 children in both population groups. In the Druze sector, the fertility rate dropped to 1.94 children per woman – a first-ever dip below 2.0 children – while in the Muslim sector fertility rates have steadily declined, reaching 2.99 in 2020. For “other” women (primarily those who are not Jewish according to religious law), the fertility rate sank below 1.5 children per woman.

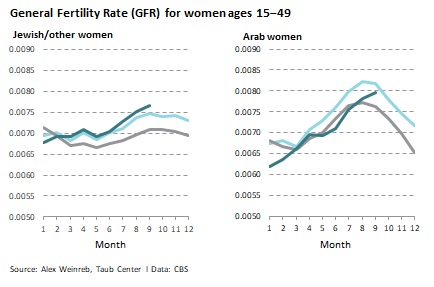

The Covid–19 crisis led to a rise in fertility rates among Jewish women in Israel: In many countries, the pandemic resulted in lower fertility rates. Demographers agree that, in most cases, the crisis accelerated trends that had been in place during the pre-Covid-19 period, and that fertility rates may be expected to fall even lower in 2021 in those countries where a downward trend had already been observed, reaching unprecedented lows, for example, below 1.6 in the US and the UK. For Jewish women in Israel, by contrast, the reaction has been different, and a rise in fertility rates has been observed. Births up to December 2020 were the result of pre-pandemic conceptions, and the general fertility rate for Jewish and other women was below that of 2019. By March 2021, however, the general fertility rate had climbed above the 2019 level, and between March and September 2021 there was a rise of 6% in the number of births to Jewish and Other women. The general fertility rate for Arab Israeli women dropped until February 2021, after which it recovered slightly, but overall it has remained below the 2019 rate. Had the pandemic not erupted, the fertility rate of Arab Israeli women would likely have fallen even lower.

We do not yet know whether the upswing in Jewish women’s fertility rates reflects a change in timing of fertility (parents had planned to have a child a year later anyway) rather than a true “baby boom” (parents giving birth to an extra child they had not planned). In either case, the acceleration will have long-term effects on the size of a given age cohort, which in turn will have an impact on education and the labor market.

Immigration to Israel has grown in recent years, but the Covid-19 crisis did not lead to further rises: Net immigration to Israel has risen over the past 15 years, due to rising immigrant numbers and lower emigrant numbers. During the period 2015-2019, total immigration ranged from 26,000 to 33,000 persons per year. The Covid-19 pandemic led to a sharp reduction in immigration to Israel; the figure for 2020 was 19,700, with the decline attributable to lower immigration from Russia and the Ukraine. Across the first 11 months of 2021, the number of immigrants recovered but was lower than in 2019. This is surprising given the Israeli government’s expectations of a large immigration wave known as “Corona Zionism.” These expectations were based on a rise in the number of immigration files opened, and on growing interest in Israeli real estate on the part of foreign buyers impressed by Israel’s relatively successful handling of the pandemic in its early stages. Likewise, no major wave of returning residents was observed in the wake of the pandemic.

How Many Deaths Could Potentially Be Prevented in Israel?

Prof. Alex Weinreb, Elon Seela

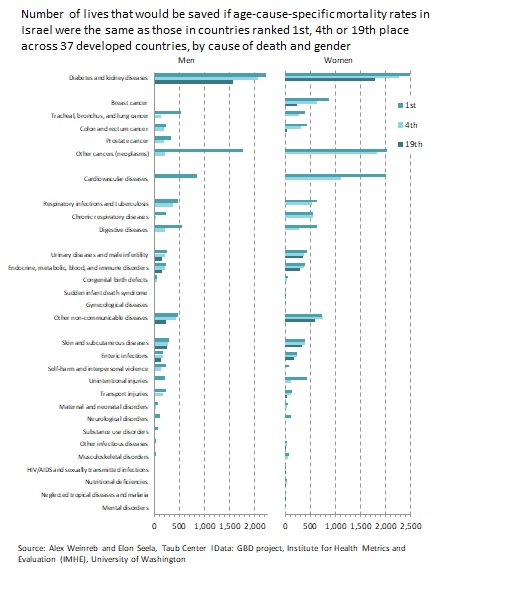

Between 1975 and 2018, Israel’s life expectancy at birth rose from 72 to almost 83 years (a three-month addition per year), bringing Israel from 17th place to 5th place in the OECD. The increase resulted from a near-total cessation of mortality from infectious disease at early ages, and from a drop in mortality from chronic disease, as well as from advancements in medical science, clinical treatment, and health behavior. In a new Taub Center study comparing cause-of-death data across 37 developed countries, the researchers sought to identify areas on which Israel should focus in order to continue reducing mortality rates based on current conditions, that is, assuming no further technological advances or medical breakthroughs.

Israel lags behind the rest of the world in diabetes treatment and in survival rates for several types of cancer: A third of Israeli deaths result from malignancies, a quarter from heart disease, and 11% from diabetes. In international comparison, Israel ranks high in terms of its mortality rate from the five most common causes (apart from diabetes) – that is, its mortality rate from these causes is relatively low. However, Israel lags behind most other countries in diabetes treatment; its mortality rate from this disease puts it in 35th place for women, and 36th place for men, in the 37-country sample. Taub Center research indicates that, were Israel’s diabetes mortality rates by age identical to those of the mid-ranked nations, total mortality would drop by 7% per year. Furthermore, although Israel ranks relatively high for cancer survival, its performance is lower for certain types of cancer, especially those that affect women. Across the 37 countries, women are in 32nd place for breast cancer, and 23rd place for colorectal cancer. Israel is also at the bottom of the rankings on some causes of death with lower prevalence, such as infectious intestinal disease, metabolic and immune system disorders, and endocrine disorders.

Appropriate investment would reduce health inequality between different populations: The data point to several health-related areas where investment in particular populations, whether through changing clinical practice, public health resources, or promoting behavioral change, would reduce both overall mortality and health inequality between different populations. For example, the Arab Israeli sector’s diabetes rate is three times higher than that of the Jewish sector, while the incidence of lung cancer among Arab Israeli men is 50% higher than among Jewish men – although the Jewish women’s lung cancer rate is 150% higher than that of Arab Israeli women. The Haredi sector displays low rates of pregnancy testing and breast cancer screening. Finally, behavioral change can produce a number of positive outcomes simultaneously. For example, improved nutrition may reduce diabetes risk factors while also lowering the risk of cardiovascular events and certain types of cancer, while frequent and comprehensive screening may detect clinical conditions at early stages when they are easily treated.

The Taub Center for Social Policy Studies in Israel is an independent, non-partisan socioeconomic research institute. The Center provides decision makers and the public with research and findings on some of the most critical issues facing Israel in the areas of education, health, welfare, labor markets and economic policy in order to impact the decision-making process in Israel and to advance the well-being of all Israelis.